Bayesian modelling

Variational inference

Last compiled Tuesday Apr 15, 2025

Variational inference

Laplace approximation provides a heuristic for large-sample approximations, but it fails to characterize well \(p(\boldsymbol{\theta} \mid \boldsymbol{y})\).

We consider rather a setting where we approximate \(p\) by another distribution \(g\) which we wish to be close.

The terminology variational is synonym for optimization in this context.

Kullback–Leibler divergence

The Kullback–Leibler divergence between densities \(f_t(\cdot)\) and \(g(\cdot; \boldsymbol{\psi}),\) is \[\begin{align*} \mathsf{KL}(f_t \parallel g) &=\int \log \left(\frac{f_t(\boldsymbol{x})}{g(\boldsymbol{x}; \boldsymbol{\psi})}\right) f_t(\boldsymbol{x}) \mathrm{d} \boldsymbol{x}\\ &= \int \log f_t(\boldsymbol{x}) f_t(\boldsymbol{x}) \mathrm{d} \boldsymbol{x} - \int \log g(\boldsymbol{x}; \boldsymbol{\psi}) f_t(\boldsymbol{x}) \mathrm{d} \boldsymbol{x} \\ &= {\color{#c38f16}{\mathsf{E}_{f_t}\{\log f_t(\boldsymbol{X})\}}} - \mathsf{E}_{f_t}\{\log g(\boldsymbol{X}; \boldsymbol{\psi})\} \end{align*}\] The \({\color{#c38f16}{\text{negative entropy}}}\) does not depend on \(g(\cdot).\)

Model misspecification

- The divergence is strictly positive unless \(g(\cdot; \boldsymbol{\psi}) \equiv f_t(\cdot).\)

- The divergence is not symmetric.

The Kullback–Leibler divergence notion is central to study of model misspecification.

- if we fit \(g(\cdot)\) when data arise from \(f_t,\) the maximum likelihood estimator of the parameters \(\widehat{\boldsymbol{\psi}}\) will be the value of the parameter that minimizes the Kullback–Leibler divergence \(\mathsf{KL}(f_t \parallel g)\).

Marginal likelihood

Consider now the problem of approximating the marginal likelihood, sometimes called the evidence, \[\begin{align*} p(\boldsymbol{y}) = \int_{\boldsymbol{\Theta}} p(\boldsymbol{y}, \boldsymbol{\theta}) \mathrm{d} \boldsymbol{\theta}. \end{align*}\] where we only have the joint \(p(\boldsymbol{y}, \boldsymbol{\theta})\) is the product of the likelihood times the prior.

Approximating the marginal likelihood

Consider \(g(\boldsymbol{\theta};\boldsymbol{\psi})\) with \(\boldsymbol{\psi} \in \mathbb{R}^J\) an approximating density function

- whose integral is one over \(\boldsymbol{\Theta} \subseteq \mathbb{R}^p\) (normalized density)

- whose support is part of that of \(\mathrm{supp} (g) \subseteq \mathrm{supp}(p) = \boldsymbol{\Theta}\) (so KL divergence is not infinite)

Objective: minimize the Kullback–Leibler divergence \[\mathsf{KL}\left\{p(\boldsymbol{\theta} \mid \boldsymbol{y}) \parallel g(\boldsymbol{\theta};\boldsymbol{\psi})\right\}.\]

Problems ahead

Minimizing the Kullback–Leibler divergence is not feasible to evaluate the posterior.

Taking \(f_t = p(\boldsymbol{\theta} \mid \boldsymbol{y})\) is not feasible: we need the marginal likelihood to compute the expectation!

Alternative expression for the marginal likelihood

We consider a different objective to bound the marginal likelihood. Write

\[\begin{align*} p(\boldsymbol{y}) = \int_{\boldsymbol{\Theta}} \frac{p(\boldsymbol{y}, \boldsymbol{\theta})}{g(\boldsymbol{\theta};\boldsymbol{\psi})} g(\boldsymbol{\theta};\boldsymbol{\psi}) \mathrm{d} \boldsymbol{\theta}. \end{align*}\]

Bounding the marginal likelihood

For \(h(x)\) a convex function, Jensen’s inequality implies that \[h\{\mathsf{E}(X)\} \leq \mathsf{E}\{h(X)\},\] and applying this with \(h(x)=-\log(x),\) we get \[\begin{align*} -\log p(\boldsymbol{y}) \leq -\int_{\boldsymbol{\Theta}} \log \left(\frac{p(\boldsymbol{y}, \boldsymbol{\theta})}{g(\boldsymbol{\theta};\boldsymbol{\psi})}\right) g(\boldsymbol{\theta};\boldsymbol{\psi}) \mathrm{d} \boldsymbol{\theta}. \end{align*}\]

Evidence lower bound

We can thus consider the model that minimizes the reverse Kullback–Leibler divergence \[\begin{align*} g(\boldsymbol{\theta}; \widehat{\boldsymbol{\psi}}) = \mathrm{argmin}_{\boldsymbol{\psi}} \mathsf{KL}\{g(\boldsymbol{\theta};\boldsymbol{\psi}) \parallel p(\boldsymbol{\theta} \mid \boldsymbol{y})\}. \end{align*}\]

Since \(p(\boldsymbol{\theta}, \boldsymbol{y}) = p(\boldsymbol{\theta} \mid \boldsymbol{y}) p(\boldsymbol{y})\), \[\begin{align*} \mathsf{KL}\{g(\boldsymbol{\theta};\boldsymbol{\psi}) \parallel p(\boldsymbol{\theta} \mid \boldsymbol{y})\} &= \mathsf{E}_{g}\{\log g(\boldsymbol{\theta})\} - \mathsf{E}_g\{\log p( \boldsymbol{\theta}, \boldsymbol{y})\} \\&\quad+ \log p(\boldsymbol{y}). \end{align*}\]

Evidence lower bound

Instead of minimizing the Kullback–Leibler divergence, we can equivalently maximize the so-called evidence lower bound (ELBO) \[\begin{align*} \mathsf{ELBO}(g) = \mathsf{E}_g\{\log p(\boldsymbol{y}, \boldsymbol{\theta})\} - \mathsf{E}_{g}\{\log g(\boldsymbol{\theta})\} \end{align*}\]

The ELBO is a lower bound for the marginal likelihood because a Kullback–Leibler divergence is non-negative and \[\begin{align*} \log p(\boldsymbol{y}) = \mathsf{ELBO}(g) + \mathsf{KL}\{g(\boldsymbol{\theta};\boldsymbol{\psi}) \parallel p(\boldsymbol{\theta} \mid \boldsymbol{y})\}. \end{align*}\]

Use of ELBO

The idea is that we will approximate the density \[p(\boldsymbol{\theta} \mid \boldsymbol{y}) \approx g(\boldsymbol{\theta}; \widehat{\boldsymbol{\psi}}).\]

- the ELBO can be used for model comparison (but we compare bounds…)

- we can sample from \(q\) as before.

Heuristics of ELBO

Maximize the evidence, subject to a regularization term: \[\begin{align*} \mathsf{ELBO}(g) = \mathsf{E}_g\{\log p(\boldsymbol{y}, \boldsymbol{\theta})\} - \mathsf{E}_{g}\{\log g(\boldsymbol{\theta})\} \end{align*}\]

The ELBO is an objective function comprising:

- the first term will be maximized by taking a distribution placing mass near the MAP of \(p(\boldsymbol{y}, \boldsymbol{\theta}),\)

- the second term can be viewed as a penalty that favours high entropy of the approximating family (higher for distributions which are diffuse).

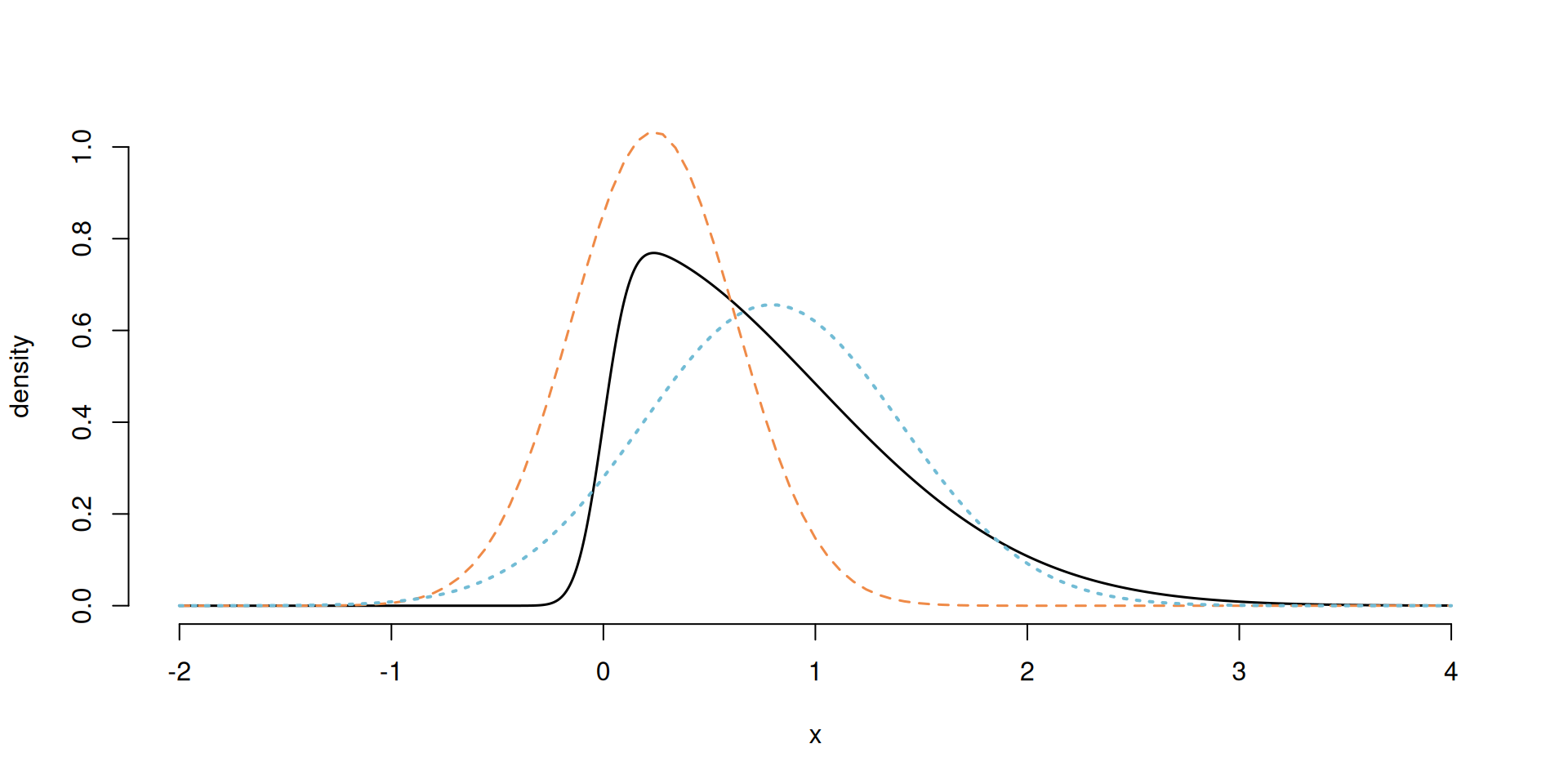

Laplace vs variational approximation

Figure 1: Skewed density with the Laplace approximation (dashed orange) and variational Gaussian approximation (dotted blue).

Choice of approximating density

In practice, the quality of the approximation depends on the choice of \(g(\cdot; \boldsymbol{\psi}).\)

- We typically want matching support.

- The approximation will be affected by the correlation between posterior components \(\boldsymbol{\theta} \mid \boldsymbol{y}.\)

- Derivations can also be done for \((\boldsymbol{U}, \boldsymbol{\theta})\), where \(\boldsymbol{U}\) are latent variables from a data augmentation scheme.

Factorization

We can consider densities \(g(;\boldsymbol{\psi})\) that factorize into blocks with parameters \(\boldsymbol{\psi}_1, \ldots, \boldsymbol{\psi}_M,\) where \[\begin{align*} g(\boldsymbol{\theta}; \boldsymbol{\psi}) = \prod_{j=1}^M g_j(\boldsymbol{\theta}_j; \boldsymbol{\psi}_j) \end{align*}\] If we assume that each of the \(J\) parameters \(\theta_1, \ldots, \theta_J\) are independent, then we obtain a mean-field approximation.

Maximizing the ELBO one step at a time

\[\begin{align*} \mathsf{ELBO}(g) &= \int \log p(\boldsymbol{y}, \boldsymbol{\theta}) \prod_{j=1}^M g_j(\boldsymbol{\theta}_j)\mathrm{d} \boldsymbol{\theta} \\&\quad- \sum_{j=1}^M \int \log \{ g_j(\boldsymbol{\theta}_j) \} g_j(\boldsymbol{\theta}_j) \mathrm{d} \boldsymbol{\theta}_j \\& \stackrel{\boldsymbol{\theta}_i}{\propto} \mathsf{E}_{i}\left[\mathsf{E}_{-i}\left\{\log p(\boldsymbol{y}, \boldsymbol{\theta})\right\} \right] - \mathsf{E}_i\left[\log \{ g_i(\boldsymbol{\theta}_i) \}\right] \end{align*}\] which is the negative of a Kullback–Leibler divergence.

Optimal choice of approximating density

The maximum possible value of zero for the KL is attained when \[\log \{ g_i(\boldsymbol{\theta}_i) \} = \mathsf{E}_{-i}\left\{\log p(\boldsymbol{y}, \boldsymbol{\theta})\right\}.\] The choice of marginal \(g_i\) that maximizes the ELBO is \[\begin{align*} g^{\star}_i(\boldsymbol{\theta}_i) \propto \exp \left[ \mathsf{E}_{-i}\left\{\log p(\boldsymbol{y}, \boldsymbol{\theta})\right\}\right]. \end{align*}\] Often, we look at the kernel of \(g^{\star}_j\) to deduce the normalizing constant.

Coordinate-ascent variational inference (CAVI)

- We can maximize \(g^{\star}_j\) in turn for each \(j=1, \ldots, M\) treating the other parameters as fixed.

- This scheme is guaranteed to monotonically increase the ELBO until convergence to a local maximum.

- Convergence: monitor ELBO and stop when the change is lower then some present numerical tolerance.

- The approximation may have multiple local optima: perform random initializations and keep the best one.

Example of CAVI mean-field for Gaussian target

We consider the example from Section 2.2.2 of Ormerod & Wand (2010) for approximation of a Gaussian distribution, with \[\begin{align*} Y_i &\sim \mathsf{Gauss}(\mu, \tau^{-1}), \qquad i =1, \ldots, n;\\ \mu &\sim \mathsf{Gauss}\{\mu_0, (\tau\tau_0)^{-1}\} \\ \tau &\sim \mathsf{gamma}(a_0, b_0). \end{align*}\] This is an example where the full posterior is available in closed-form, so we can compare our approximation with the truth.

Variational approximation to Gaussian — mean

We assume a factorization of the variational approximation \(g_\mu(\mu)g_\tau(\tau);\) the factor for \(g_\mu\) is proportional to \[\begin{align*} \log g^{\star}_{\mu}(\mu) \propto -\frac{\mathsf{E}_{\tau}(\tau)}{2} \left\{ \sum_{i=1}^n (y_i-\mu)^2-\frac{\tau_0}{2}(\mu-\mu_0)^2\right\}, \end{align*}\] which is quadratic in \(\mu\) and thus must be Gaussian with precision \(\tau_n = \mathsf{E}_{\tau}(\tau)(\tau_0 + n)\) and mean \(\tau_0\mu_0 +n\overline{y}.\)

Variational approximation to Gaussian — precision

The optimal precision factor satisfies \[\begin{align*} \ln g^{\star}_{\tau}(\tau) &\propto \log \tau\left(\frac{n+1}{2} + a_0-1\right) - \tau b_n\\ b_n & = b_0 + \frac{\mathsf{E}_{\mu}\left\{\sum_{i=1}^n (y_i-\mu)^2\right\} + \tau_0\mathsf{E}{\mu}\left\{(\mu-\mu_0)^2\right\}}{2} \end{align*}\] Thus a gamma with shape \(a_n =a_0 + (n+1)/2\) and rate \(b_n\).

Rate of the gamma for \(g_\tau\)

It is helpful to rewrite the expected value as \[\begin{align*} \mathsf{E}_{\mu}\left\{\sum_{i=1}^n (y_i-\mu)^2\right\} = \sum_{i=1}^n \{y_i - \mathsf{E}_{\mu}(\mu)\}^2 + n \mathsf{Var}_{\mu}(\mu), \end{align*}\] so that it depends on the parameters of the distribution of \(\mu\) directly.

CAVI for Gaussian

The algorithm cycles through the following updates until convergence:

- \(\mathsf{Va}_{\mu}(\mu) = \{\mathsf{E}_{\tau}(\tau)(\tau_0 + n )\}^{-1},\)

- \(\mathsf{E}_{\mu}(\mu) = \mathsf{Va}_{\mu}(\mu)\{\tau_0\mu_0 + n \overline{y}\},\)

- \(\mathsf{E}_{\tau}(\tau) = a_n/b_n\) where \(b_n\) is a function of both \(\mathsf{E}_{\mu}(\mu)\) and \(\mathsf{Var}_{\mu}(\mu).\)

We only compute the ELBO at the end of each cycle.

Maximization?

Recall that alternating these steps is equivalent to maximization of the ELBO.

- each iteration performs conditional optimization implicitly (as we minimize the reverse KL divergence).

Monitoring convergence

The derivation of the ELBO is straightforward but tedious; \[\begin{align*} \mathsf{ELBO}(g) & = a_0\log(b_0) -a_n\log b_n + \log \{\Gamma(a_n)/\Gamma(a_0)\} \\& \quad - \frac{n}{2}\log(2\pi)+ \frac{1 + \log (\tau_0/\tau_n)}{2}. \end{align*}\]

We can also consider relative changes in parameter values as tolerance criterion.

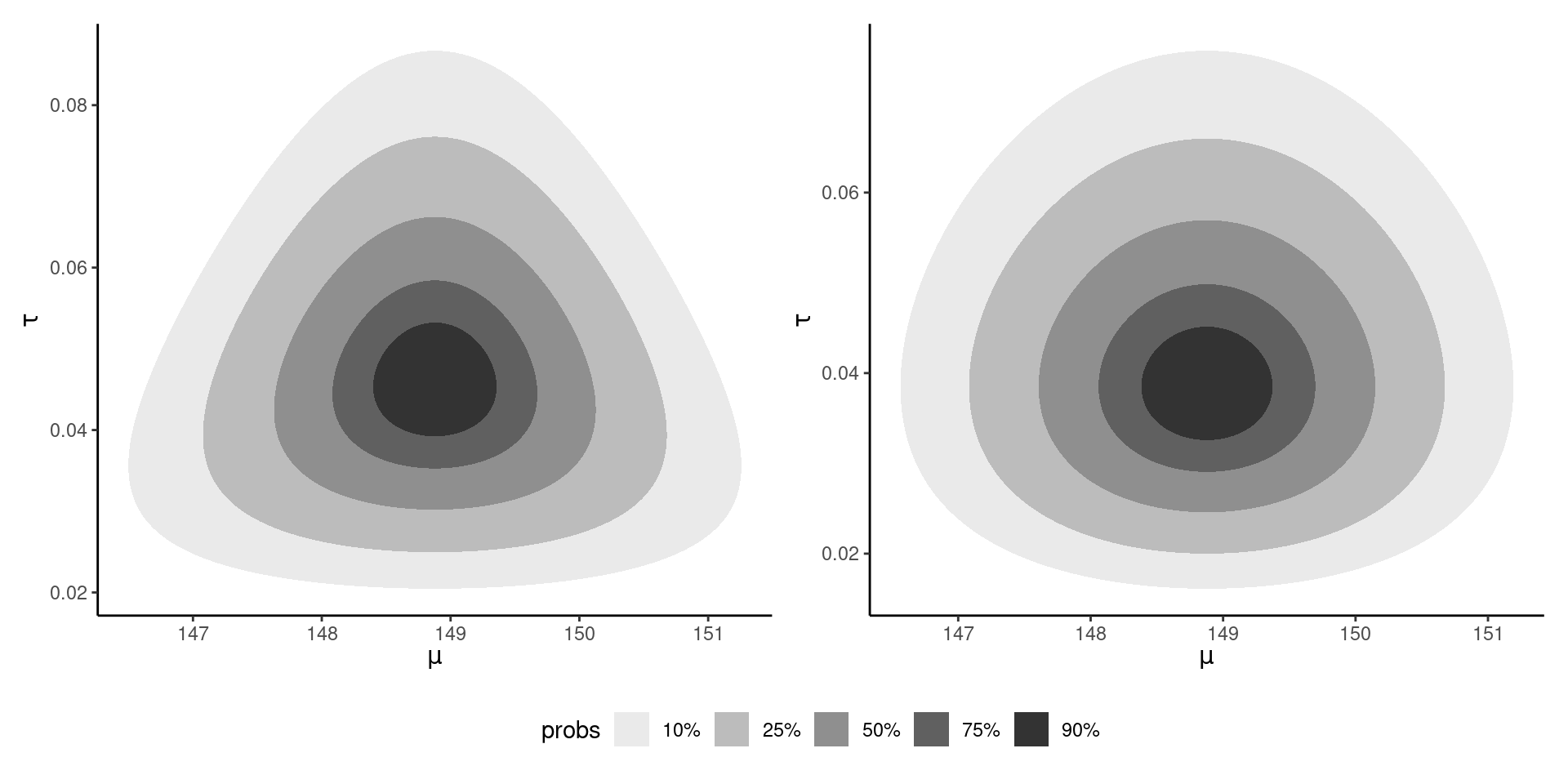

Bivariate posterior density

Figure 2: Bivariate density posterior for the conjugate Gaussian-gamma model (left) and CAVI approximation (right).

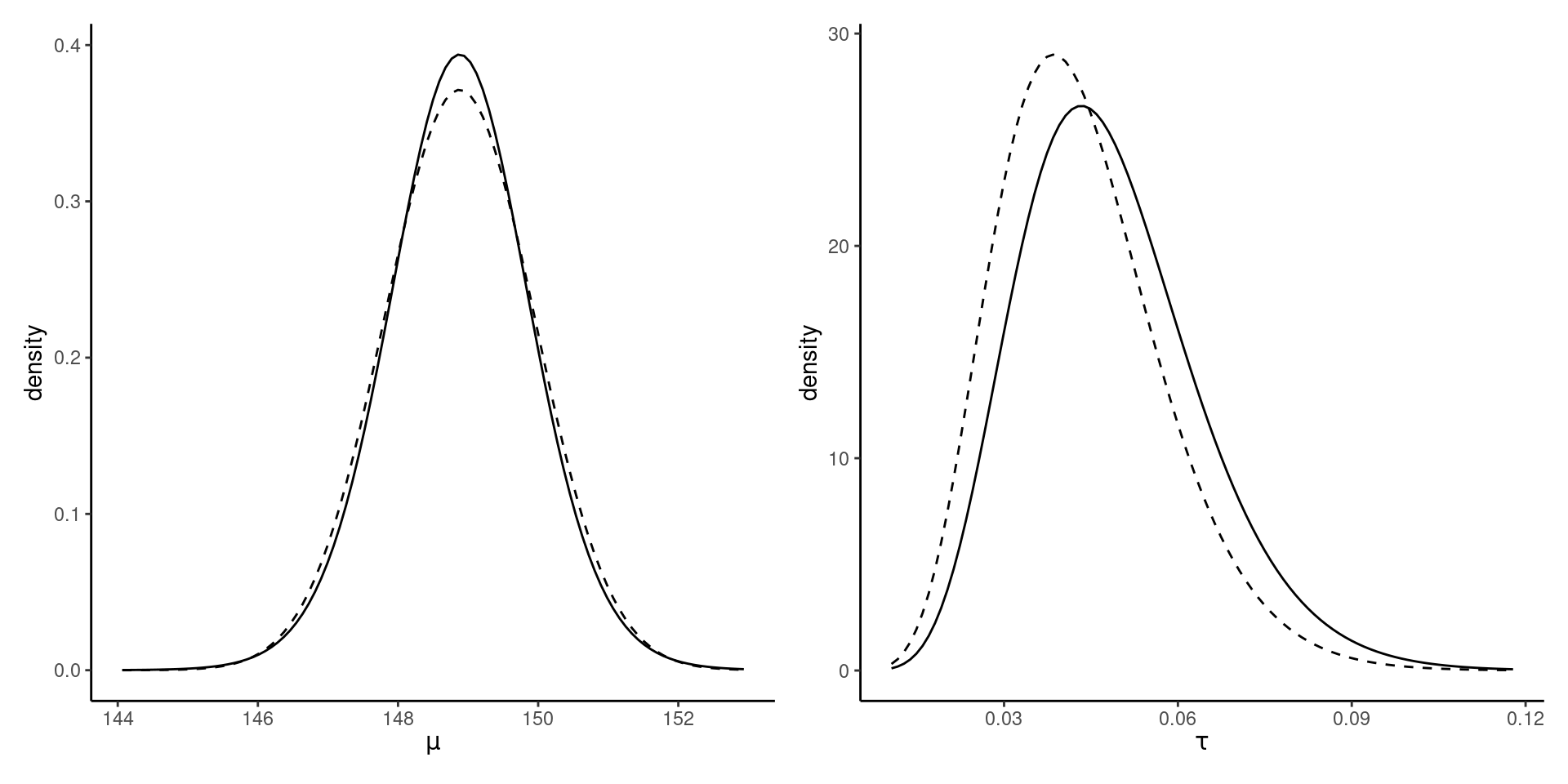

Marginal posterior densities

Figure 3: Marginal posterior density of the mean and precision of the Gaussian (full line), with CAVI approximation (dashed).

CAVI for probit regression

A probit regression is a generalized linear model with probability of success \(\Phi(\mathbf{x}_i\boldsymbol{\beta}),\) where \(\Phi(\cdot)\) is the cumulative distribution function of a standard Gaussian variable.

We can write the model as \[\begin{align*} p(\boldsymbol{y} \mid \boldsymbol{\beta}) = \Phi(\mathbf{X}\boldsymbol{\beta})^{\boldsymbol{y}}\Phi(-\mathbf{X}\boldsymbol{\beta})^{\boldsymbol{1}_n -\boldsymbol{y}} \end{align*}\] since \(1-\Phi(x) = \Phi(-x).\)

Data augmentation and CAVI

Consider data augmentation with auxiliary variables \(Z_i \mid \boldsymbol{\beta}\sim \mathsf{Gauss}(\mathbf{x}_i\boldsymbol{\beta}, 1).\)

With \(\boldsymbol{\beta} \sim \mathsf{Gauss}_p(\boldsymbol{\mu}_0, \mathbf{Q}_0^{-1}),\) the model admits conditionals \[\begin{align*} \boldsymbol{\beta} \mid \boldsymbol{Z} &\sim \mathsf{Gauss}_p\left\{\mathbf{Q}_{\boldsymbol{\beta}}^{-1}(\mathbf{X}\boldsymbol{Z} + \mathbf{Q}_0\boldsymbol{\mu}_0), \mathbf{Q}_{\boldsymbol{\beta}}^{-1} \right\} \\ Z_i \mid y_i, \boldsymbol{\beta} &\sim \mathsf{trunc. Gauss}(\mathbf{x}_i\boldsymbol{\beta}, 1, l_i, u_i) \end{align*}\] where \(\mathbf{Q}_{\boldsymbol{\beta}}= \mathbf{X}^\top\mathbf{X} + \mathbf{Q_0},\) and \([l_i, u_i]\) is \((-\infty,0)\) if \(y_i=0\) and \((0, \infty)\) if \(y_i=1.\)

CAVI factorization for probit model

We consider a factorization of the form \[g_{\boldsymbol{Z}}(\boldsymbol{z})g_{\boldsymbol{\beta}}(\boldsymbol{\beta}).\]

Then, the optimal form of the density further factorizes as \[g_{\boldsymbol{Z}}(\boldsymbol{z}) = \prod_{i=1}^n g_{Z_i}(z_i).\]

Gibbs, EM and CAVI

- We exploit the conditionals in the same way as for Gibbs sampling

- The only difference is that we substitute unknown parameter functionals by their expectations.

- Also deep links with the expectation-maximization (EM) algorithm, which optimizes at each step parameters after replacing the log posterior of augmented data by their expectation.

- CAVI however fixes the parameter values (less uncertainty in the posterior because of that).

Updates for CAVI - probit regression

The model depends on

- \(\mu_{\boldsymbol{Z}}\), the mean parameter of \(\boldsymbol{Z}\)

- \(\mu_{\boldsymbol{\beta}},\) the mean of \(\boldsymbol{\beta}.\)

Consider the terms in the posterior proportional to \(Z_i\), where \[\begin{align*} p(z_i \mid \boldsymbol{\beta}, y_i) \propto -\frac{z_i^2 - 2z_i \mathbf{x}_i\boldsymbol{\beta}}{2} \times \mathrm{I}(z_i >0)^{y_i}\mathrm{I}(z_i <0)^{1-y_i} \end{align*}\] which is linear in \(\boldsymbol{\beta}\).

Truncated Gaussian

The expectation of a univariate truncated Gaussian \(Z \sim \mathsf{trunc. Gauss}(\mu,\sigma^2, l, u)\) is \[\begin{align*} \mathsf{E}(Z) = \mu - \sigma\frac{\phi\{(u-\mu/\sigma)\} - \phi\{(l-\mu/\sigma)\}}{\Phi\{(u-\mu/\sigma)\} - \Phi\{(l-\mu/\sigma)\}}. \end{align*}\]

Update for CAVI

If we replace \(\mu=\mathbf{x}_i\mu_{\boldsymbol{\beta}}\), we get the update \[\begin{align*} \mu_{Z_i}(z_i) = \begin{cases} \mathbf{x}_i\mu_{\boldsymbol{\beta}} - \frac{ \phi(\mathbf{x}_i\mu_{\boldsymbol{\beta}})}{1-\Phi(\mathbf{x}_i\mu_{\boldsymbol{\beta}})} & y_i = 0;\\ \mathbf{x}_i\mu_{\boldsymbol{\beta}} + \frac{ \phi(\mathbf{x}_i\mu_{\boldsymbol{\beta}})}{\Phi(\mathbf{x}_i\mu_{\boldsymbol{\beta}})} & y_i = 1, \end{cases} \end{align*}\] since \(\phi(x)=\phi(-x).\)

Update for regression parameters

The optimal form for \(\boldsymbol{\beta}\) is Gaussian and proceeding similarly, \[\begin{align*} \boldsymbol{\mu}_{\boldsymbol{\beta}} = (\mathbf{X}^\top\mathbf{X} + \mathbf{Q_0})^{-1}(\mathbf{X}\boldsymbol{\mu}_{\boldsymbol{Z}} + \mathbf{Q}_0\boldsymbol{\mu}_0) \end{align*}\] where \(\boldsymbol{\mu}_{\boldsymbol{Z}} = \mathsf{E}_{\boldsymbol{Z}}(\boldsymbol{Z}).\)

Other parameters of the distribution are known functions of covariates, etc.

Example

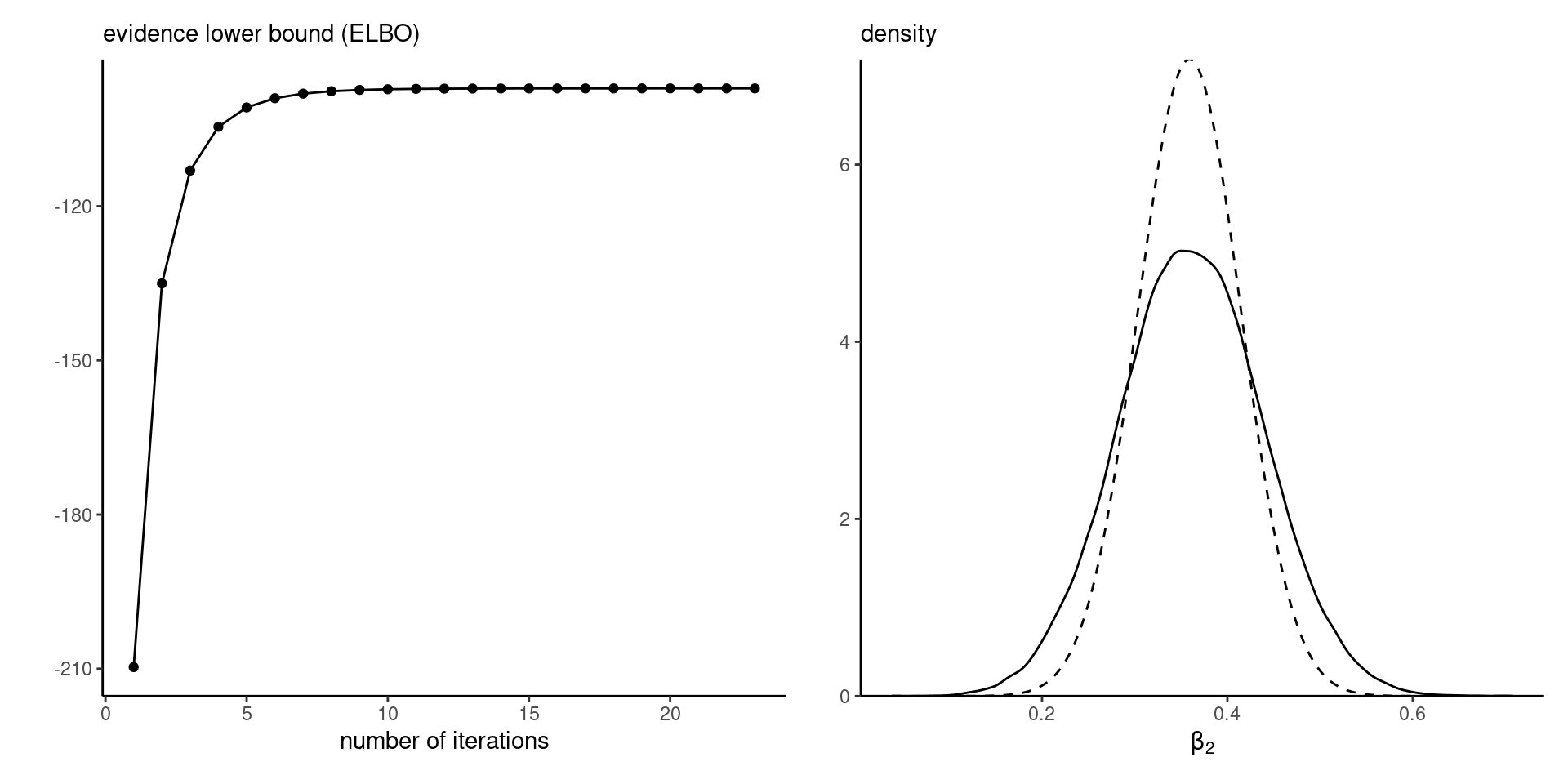

We consider for illustration purposes data from Experiment 2 of Duke & Amir (2023) on the effect of sequential decisions and purchasing formats.

We fit a model with - age of the participant (scaled) and - format, the binary variable which indicate the experimental condition (sequential vs integrated).

ELBO and marginal density approximation

Figure 4: ELBO (left) and marginal density approximation with true density (full) versus variational approximation (dashed).

Stochastic optimization

We consider alternative numeric schemes which rely on stochastic optimization (Hoffman et al., 2013).

The key idea behind these methods is that

- we can use gradient-based algorithms,

- and approximate the expectations with respect to \(g\) by drawing samples from it

Also allows for minibatch (random subset) selection to reduce computational costs in large samples

Stochastic gradient descent

Consider \(f(\boldsymbol{\theta})\) a differentiable function with gradient \(\nabla f(\boldsymbol{\theta})\) and \(\rho_t\) a Robbins–Munro sequence.

To maximize \(f(\boldsymbol{\theta})\), we construct a series of first-order approximations starting from \(\boldsymbol{\theta}^{(0)}\) with \[\begin{align*} \boldsymbol{\theta}^{(t)} = \boldsymbol{\theta}^{(t-1)} +\rho_t \mathsf{E}\left\{\nabla f(\boldsymbol{\theta}^{(t-1)})\right\}. \end{align*}\] where the expected value is evaluated via Monte Carlo, until changes in \(\|\boldsymbol{\theta}_{t} - \boldsymbol{\theta}_{t-1}\|\) is less than some tolerance value.

Robbins–Munro sequence

The step sizes must satisfy \[\sum_{t=1}^\infty \rho_t = \infty, \qquad\sum_{t=1}^\infty \rho^2_t< \infty.\]

Parameter-specific scaling helps with updates of parameters on very different scales.

Black-box variational inference

Ranganath et al. (2014) shows that the gradient of the ELBO reduces to \[\begin{align*} \frac{\partial}{\partial \boldsymbol{\psi}} \mathsf{ELBO}(g) &=\mathsf{E}_{g}\left\{\frac{\partial \log g(\boldsymbol{\theta}; \boldsymbol{\psi})}{\partial \boldsymbol{\psi}} \times \log \left( \frac{p(\boldsymbol{\theta}, \boldsymbol{y})}{g(\boldsymbol{\theta}; \boldsymbol{\psi})}\right)\right\} \end{align*}\] using the change rule, differentiation under the integral sign (dominated convergence theorem) and the identity \[\begin{align*} \frac{\partial \log g(\boldsymbol{\theta}; \boldsymbol{\psi})}{\partial \boldsymbol{\psi}} g(\boldsymbol{\theta}; \boldsymbol{\psi}) = \frac{\partial g(\boldsymbol{\theta}; \boldsymbol{\psi})}{\partial \boldsymbol{\psi}} \end{align*}\]

Black-box variational inference in practice

- Note that the gradient simplifies for \(g_i\) in exponential families.

- The gradient estimator is particularly noisy, so Ranganath et al. (2014) provide two methods to reduce the variance of this expression using control variates and Rao–Blackwellization.

Automatic differentiation variational inference

Kucukelbir et al. (2017) proposes a stochastic gradient algorithm, but with two main innovations.

- The first is the general use of Gaussian approximating densities for factorized density, with parameter transformations to map from the support of \(T: \boldsymbol{\Theta} \mapsto \mathbb{R}^p\) via \(T(\boldsymbol{\theta})=\boldsymbol{\zeta}.\)

- The second is to use the resulting location-scale family to obtain an alternative form of the gradient.

Gaussian full-rank approximation

Consider an approximation \(g(\boldsymbol{\theta}; \boldsymbol{\psi})\) where \(\boldsymbol{\psi}\) consists of

- mean parameters \(\boldsymbol{\mu}\) and

- covariance \(\boldsymbol{\Sigma}\), parametrized through a Cholesky decomposition

The full approximation is of course more flexible, but is more expensive to compute than the mean-field approximation.

Gaussian entropy

The entropy of the multivariate Gaussian with mean \(\boldsymbol{\mu}\) and covariance \(\boldsymbol{\Sigma} = \mathbf{LL}^\top\), where \(\mathbf{L}\) is a lower triangular matrix, is \[\begin{align*} \mathcal{E}(\mathbf{L}) = - \mathsf{E}_g(\log g) &= \frac{D+D\log(2\pi) + \log |\mathbf{LL}^\top|}{2}, \end{align*}\] and only depends on \(\boldsymbol{\Sigma}\).

Eigendecomposition

We work with the matrix-log of the covariance matrix, defined through it’s eigendecomposition (or singular value decomposition) \[\boldsymbol{\Sigma}=\mathbf{V}\mathrm{diag}(\boldsymbol{\lambda})\mathbf{V}^{\top},\] where \(\mathbf{V}\) is a \(p\times p\) orthogonal matrix of eigenvectors, whose inverse is equal to it’s transpose.

Matrix-log

Most operations on the matrix only affect the eigenvalues \(\lambda_1, \ldots, \lambda_p\): the matrix-log \(\boldsymbol{\Sigma} = \exp(2\mathbf{M})\) is \[\begin{align*} \mathbf{M} =\mathbf{V}\mathrm{diag}\left\{ \frac{1}{2}\log(\boldsymbol{\lambda})\right\}\mathbf{V}^\top. \end{align*}\]

Operations on matrices

Other operations on matrices are defined analogously:

- \(\exp(\boldsymbol{\Sigma}) = \mathbf{V}\mathrm{diag}\{ \exp(\boldsymbol{\lambda})\}\mathbf{V}^\top\)

- \(\log(\boldsymbol{\Sigma}) = \mathbf{V}\mathrm{diag}\{ \log(\boldsymbol{\lambda})\}\mathbf{V}^\top\)

- The symmetrization operator is \(\mathsf{symm}(\mathbf{X}) = (\mathbf{X} + \mathbf{X}^\top)/2.\)

Gaussian scale

Since the Gaussian is a location-scale family, we can write \(\boldsymbol{\theta} = \boldsymbol{\mu} + \exp(\mathbf{M})\boldsymbol{Z},\) in terms of a standardized Gaussian, \[\begin{align*} \mathsf{ELBO} = \mathsf{E}_{\boldsymbol{Z}}\left\{ p\{\boldsymbol{y}, \boldsymbol{\theta} = \boldsymbol{\mu} + \exp(\mathbf{M})\boldsymbol{Z}\right\} + c \\\approx \frac{1}{B}\sum_{b=1}^B p\{\boldsymbol{y}, \boldsymbol{\theta} = \boldsymbol{\mu} + \exp(\mathbf{M})\boldsymbol{Z}_i\} + c \end{align*}\] for \(\boldsymbol{Z}_1, \ldots, \boldsymbol{Z}_b \sim \mathsf{Gauss}_p(\boldsymbol{0}_p, \mathbf{I}_p),\) with \(c=p\{\log(2\pi)+1\}/2 + \mathrm{trace}(\mathbf{M})\).

Gradients of the ELBO

Write the gradient of the joint log posterior density as \[\nabla p(\boldsymbol{y}, \boldsymbol{\theta}) = {\partial \log p(\boldsymbol{y}, \boldsymbol{\theta})}/{\partial \boldsymbol{\theta}}.\] Then, the gradients of the ELBO are \[\begin{align*} \frac{\partial \mathsf{ELBO}(g)}{\partial \boldsymbol{\mu}} &= \mathsf{E}_{\boldsymbol{Z}}\left\{\nabla p(\boldsymbol{y}, \boldsymbol{\theta})\right\} \\ \frac{\partial \mathsf{ELBO}(g)}{\partial \mathbf{M}} &= \mathsf{symm}\left[\mathsf{E}_{\boldsymbol{Z}}\left\{\nabla p(\boldsymbol{y}, \boldsymbol{\theta})\boldsymbol{Z}^\top\exp(\mathbf{M})\right\}\right] + \mathbf{I}_p. \end{align*}\]

Gradients of ELBO for location-scale families

We can rewrite the expression for the gradient with respect to the matrix-log \(\mathbf{M}\) using integration by part \[\begin{align*} &\mathsf{E}_{\boldsymbol{Z}}\left[\frac{\partial \log p\{\boldsymbol{y}, \boldsymbol{\theta}=\boldsymbol{\mu} + \exp(\mathbf{M})\boldsymbol{Z}\}}{\partial \boldsymbol{\theta}}\boldsymbol{Z}^\top\exp(\mathbf{M})\right] \\& =\mathsf{E}_{\boldsymbol{Z}}\left[\frac{\partial \log p\{\boldsymbol{y}, \boldsymbol{\theta}=\boldsymbol{\mu} + \exp(\mathbf{M})\boldsymbol{Z}\}}{\partial \boldsymbol{\theta}\partial \boldsymbol{\theta}^\top}\exp(2\mathbf{M})\right]. \end{align*}\] The first expression typically leads to a more noisy gradient estimator, but the second requires derivation of the Hessian.

Change of variable

The change of variable introduces a Jacobian term \(\mathbf{J}_{T^{-1}}(\boldsymbol{\zeta})\) for the approximation to the density \(p(\boldsymbol{\theta}, \boldsymbol{y})\), where

\[\begin{align*} p(\boldsymbol{\theta}, \boldsymbol{y}) = p(\boldsymbol{\zeta}, \boldsymbol{y}) \left|\mathbf{J}_{T^{-1}}(\boldsymbol{\zeta})\right| \end{align*}\] and we replace the gradient by \[\begin{align*} \nabla p(\boldsymbol{y}, \boldsymbol{\theta}) = \frac{\partial \log p(\boldsymbol{y}, \boldsymbol{\theta})}{\partial \boldsymbol{\theta}} \frac{\partial T^{-1}(\boldsymbol{\zeta})}{\partial \boldsymbol{\zeta}} + \frac{\partial \log \left|\mathbf{J}_{T^{-1}}(\boldsymbol{\zeta})\right|}{\partial \boldsymbol{\zeta}}. \end{align*}\]

Chain rule

If \(\boldsymbol{\theta} = T^{-1}(\boldsymbol{\zeta})\) and \(\boldsymbol{\zeta} = \boldsymbol{\mu} + \mathbf{L}\boldsymbol{z},\) we have for \(\boldsymbol{\psi}\) equal to either \(\boldsymbol{\mu}\) or \(\mathbf{L}\), using the chain rule, \[\begin{align*} & \frac{\partial}{\partial \boldsymbol{\psi}}\log p(\boldsymbol{y}, \boldsymbol{\theta}) \\&\quad = \frac{\partial \log p(\boldsymbol{y}, \boldsymbol{\theta})}{\partial \boldsymbol{\theta}} \times \frac{\partial T^{-1}(\boldsymbol{\zeta})}{\partial \boldsymbol{\zeta}} \times \frac{\partial (\boldsymbol{\mu} + \mathbf{L}\boldsymbol{z})}{\partial \boldsymbol{\psi}} \end{align*}\]

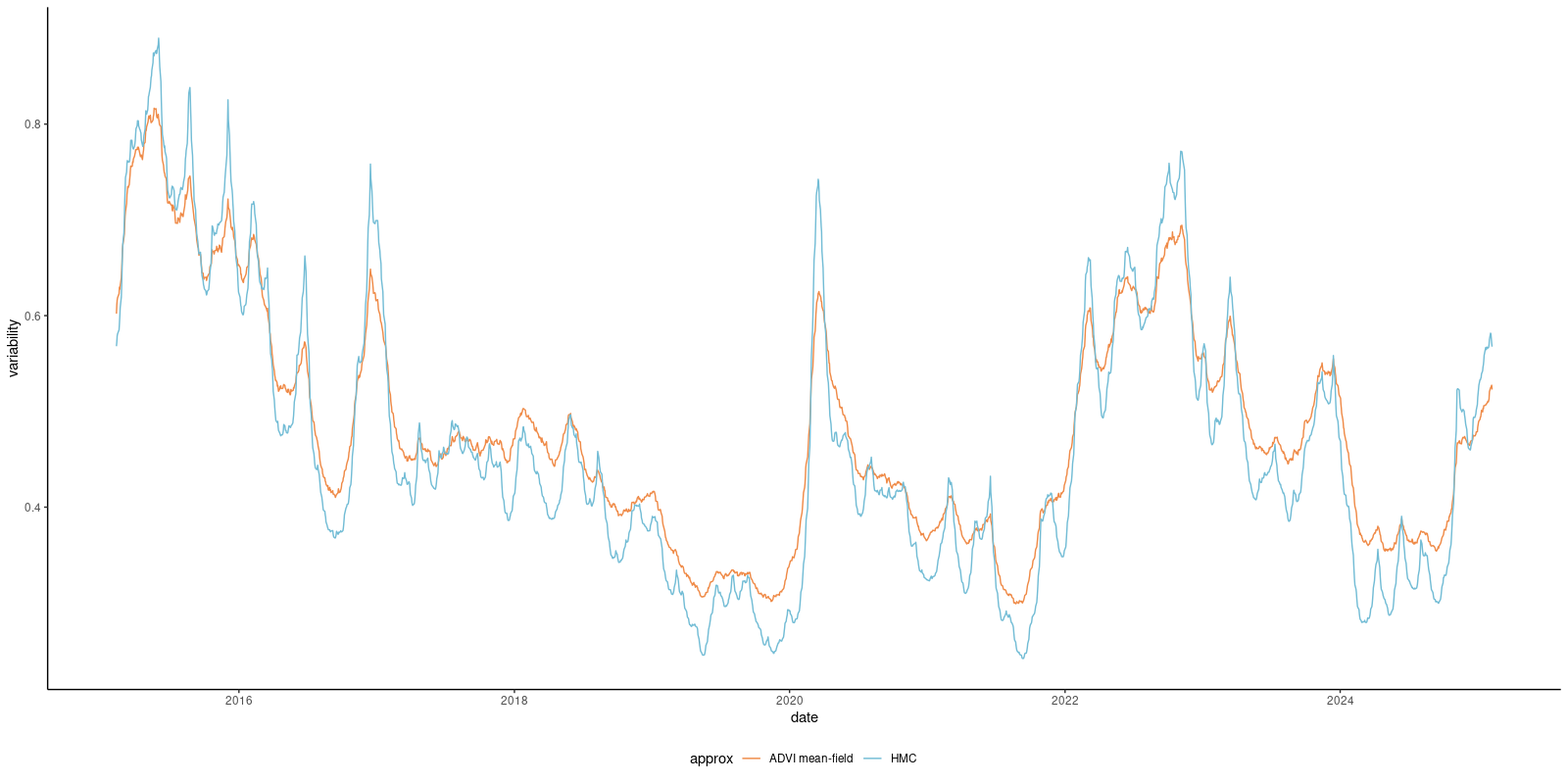

Quality of approximation

Consider the stochastic volatility model.

Fitting HMC-NUTS to the exchange rate data takes 156 seconds for 10K iterations, vs 2 seconds for the mean-field approximation.

Performance of stochastic gradient descent

The speed of convergence of the stochastic gradient descent depends on multiple factors:

- the properties of the function. Good performance is obtained for log concave distributions.

- the level of noise of the gradient estimator. Less noisy gradient estimators are preferable.

- good starting values, as the algorithm converges to a local maximum.

- the Robbins–Munro sequence used for the step size, as overly large steps may lead to divergences.

References

![]()

Comments

With vague priors, the coefficients for the mean \(\boldsymbol{\mu}_{\boldsymbol{\beta}}=(\beta_0, \beta_1, \beta_2)^\top\) matches the frequentist point estimates of the probit regression to four significant digits.

Convergence is very fast, as shown by the ELBO plot.

The marginal density approximations are underdispersed.