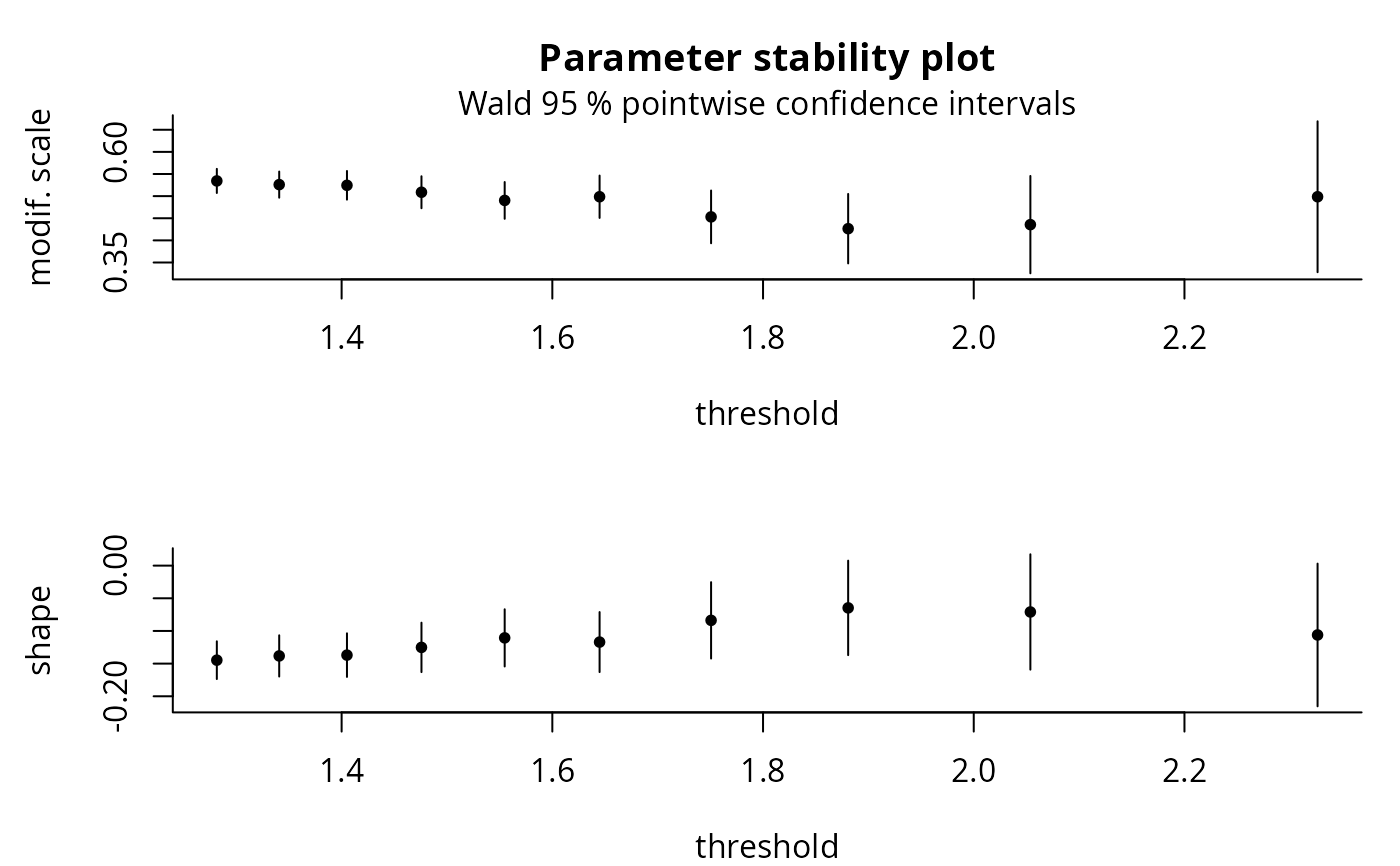

This function computes the maximum likelihood estimate at each provided threshold and plots the estimates (pointwise), along with 95% confidence/credible intervals obtained using Wald or profile confidence intervals, or else from 1000 independent draws from the posterior distribution under vague independent normal prior on the log-scale and shape. The latter two methods better reflect the asymmetry of the estimates than the Wald confidence intervals.

Arguments

- xdat

a vector of observations

- thresh

a vector of candidate thresholds at which to compute the estimates.

- method

string indicating the method for computing confidence or credible intervals. Must be one of

"wald","profile"or"post".- level

confidence level of the intervals. Default to 0.95.

- plot

logical; should parameter stability plots be displayed? Default to

TRUE.- which

character vector with elements

scaleorshape- changepar

logical; if

TRUE, changes the graphical parameters.- ...

additional arguments passed to

plot.

Value

a list with components

threshold: vector of numerical threshold values.mle: matrix of modified scale and shape maximum likelihood estimates.lower: matrix of lower bounds for the confidence or credible intervals.upper: matrix of lower bounds for the confidence or credible intervals.method: method for the confidence or coverage intervals.

plots of the modified scale and shape parameters, with pointwise confidence/credible intervals

and an invisible data frame containing the threshold thresh and the modified scale and shape parameters.

Note

The function is hard coded to prevent fitting a generalized Pareto distribution to samples of size less than 10. If the estimated shape parameters are all on the boundary of the parameter space (meaning \(\hat{\xi}=-1\)), then the plots return one-sided confidence intervals for both the modified scale and shape parameters: these typically suggest that the chosen thresholds are too high for estimation to be reliable.